Housing Market 2026: More Homes, Lower Prices—Is Now the Time to Buy?

The housing market is sending mixed signals—and for the first time in years, buyers might actually have leverage.

A recent shift shows that more homes are on the market compared to 2025, while median listing prices have dipped by approximately 2.4%. On the surface, that sounds like good news. More options, slightly lower prices, and less competition should mean opportunity.

But the real question isn’t just what’s happening—it’s what it means.

The Big Shift: Supply Is Finally Catching Up

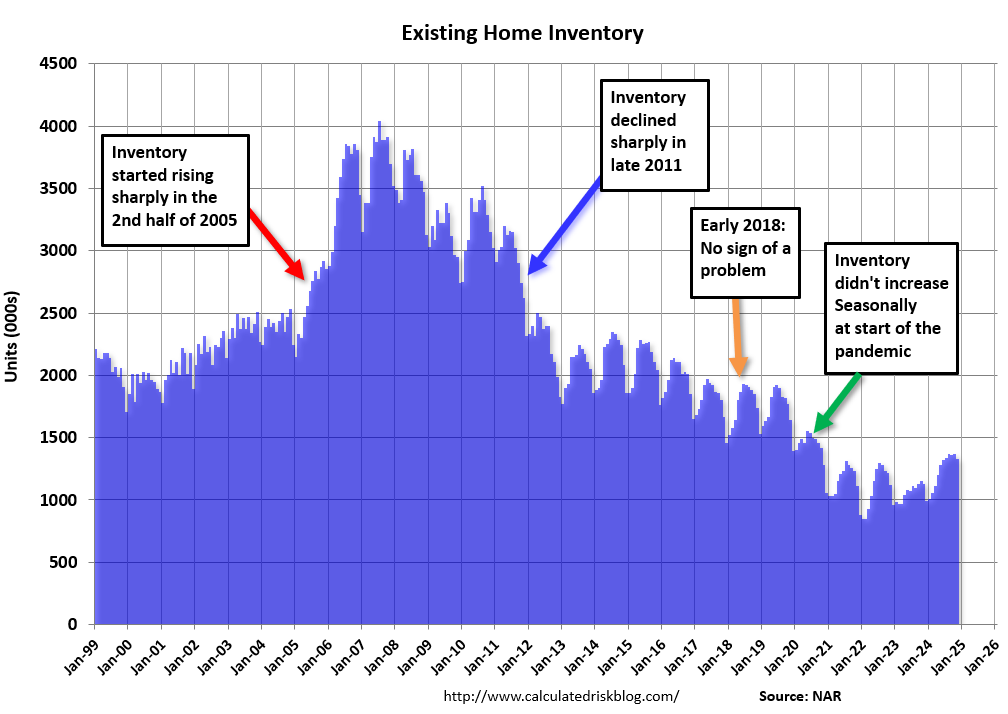

For the past few years, the U.S. housing market has been defined by scarcity. Low inventory drove bidding wars, inflated prices, and forced buyers into aggressive decisions.

Now, that dynamic is changing.

- Inventory is rising: More homeowners are listing properties, either due to life changes, financial pressure, or simply timing the market.

- Days on market are increasing: Homes aren’t flying off the shelf in 24–48 hours anymore.

- Price reductions are becoming more common: Sellers are adjusting expectations.

This shift signals a move toward a more balanced market—something buyers haven’t seen in quite some time.

Prices Are Down… But Not Crashing

A 2.4% drop in median list prices is meaningful—but it’s not a collapse.

Instead, it reflects:

- A cooling off after years of aggressive appreciation

- Sellers pricing more realistically

- Buyers regaining negotiation power

In many areas, prices are still significantly higher than pre-2020 levels. So while the market is softening, it’s far from a buyer’s paradise across the board.

What Experts Are Saying

Opinions are split, and that’s where things get interesting.

The Optimists

Some real estate professionals believe this is the window buyers have been waiting for.

Their reasoning:

- Less competition means fewer bidding wars

- More inventory gives buyers choice and leverage

- Sellers are more willing to negotiate on price, repairs, and concessions

In short: You finally have room to think before you act.

The Skeptics

Others urge caution.

Their concerns:

- Mortgage rates remain relatively high compared to historic lows

- Monthly payments are still elevated—even with slight price drops

- Economic uncertainty could impact job stability and home values

Translation: Lower prices don’t always equal affordability.

The Interest Rate Reality

Even with prices dipping slightly, interest rates are the real gatekeeper.

A small change in rates can dramatically impact monthly payments. For example:

- A 1% increase in mortgage rates can raise a monthly payment by hundreds of dollars

- Lower home prices may not offset higher borrowing costs

This is why many buyers are still hesitant—even in a softer market.

So… Is Now the Time to Buy?

The honest answer: It depends on your situation—not the headlines.

It might be a good time if:

- You have stable income and long-term plans (5+ years)

- You’ve been priced out previously and now see opportunity

- You’re willing to negotiate and shop strategically

It might not be the right time if:

- You’re stretching financially to make the purchase work

- You’re banking on short-term appreciation

- You’re uncertain about job or location stability

The New Buyer Strategy

This isn’t the frenzy market of 2021–2022 anymore. Today’s winning strategy looks different:

- Negotiate aggressively — price, closing costs, repairs

- Take your time — don’t rush into emotional decisions

- Shop financing carefully — rates matter more than ever

- Think long-term — short-term gains are less predictable

Final Take

The housing market in 2026 is no longer one-sided. For the first time in years, buyers and sellers are meeting somewhere in the middle.

Yes, there are more homes available. Yes, prices have softened slightly. But the bigger story is this:

Power is shifting—and smart buyers are the ones who will benefit most.

If you approach this market with patience, strategy, and financial clarity, this moment could be less about timing the market—and more about positioning yourself correctly within it.